Blogs

Can Ripple (XRP) fix the issues central banks of AU and NZ face?

The main mantle of financial systems is to simplify the exchange of goods and services considering the time taken. Financial systems contain different types of institutions and procedures for enabling such settlements, and in modern economies, you will find e-money, e-payments, and legal tenders as the three available payment procedures.

The legal tender is a payment medium that is accepted by all concerned parties as a physical currency that can be used to clear credits in the same units. Generally, the physical coins and notes that serve as a legal tender are issued by a central bank, that suppliers are obliged to accept for any outstanding obligation valued in the same coinage.

E-payments are becoming the preferred mode of payment by many as each day that comes with technology advancement. Unlike physical currency, these e-payments are virtual transfers from credit and deposit accounts enabled by financial organizations like credit card firms and commercial banks. The private account ledgers and electronic platforms can only be accessed and amended by their host financial organizations.

Lastly, the third payment medium, E-money, is a virtual currency in which monetary worth is stored on software or hardware, allowing individuals to pay for commodities or services from third-party traders. E-money is more or less like cryptocurrency.

Be that as it may, for many years now, Australia’s main financial institution, has been under pressure from different quarters to modernize their medieval national remittance platform to meet the needs of the current and future economy.

With full knowledge of this need, the Reserve Bank of Australia, Australia’s central bank, actualized the New Payment Platform or NPP last year that allows individuals and businesses to make real-time settlements countrywide 24/7. The NPP offers real-time retail settlements, 24-hour service availability, and industry-wide standardization; it, however, leaves behind the complete remittance information.

Possible Ripple (XRP) Integration by Central Bank of Australia and New Zealand

Although the New Payment Platform is addressing a majority of the issues that were raised by the RBA, the settlement network is limited to domestic transactions. This leaves a huge opening for blockchain technologies and innovations such as XRP.

Fortunately for Ripple (XRP), which deals with cross-border settlements, a majority of developers working on the NPP are well aware of Ripple. Just recently, through a report done by the Reserve Bank of Australia discussing blockchain technology, Ripple managed to get positive reviews from the chief Pacific financial institution, declaring Ripple as a good alternative to Bitcoin that the report regarded as unstable.

At the moment, financial institutions of Australia and New Zealand are showing interest in RippleNet with Westpac and the National Australian Bank confirming they’re joining the Ripple network. Other relevant financial institutions such as CBA and ANZ are also showing accountable interest in RippleNet by closely monitoring the blockchain technology and are rumored to be in discussion with Ripple.

Given that all the major banks in the New Payment Platform have done trials and have experienced Ripple’s security and reliability in transferring settlements through the Ripple platform, only furthers speculations of a possible adoption of xRapid and xCurrent services shortly.

Both countries look hesitant in adopting Ripple, but given what the company has to offer, they might have to barge into the demands of the 21st century by adopting RippleNet.

For the latest cryptocurrency news, join our Telegram!

Disclaimer: This article should not be taken as, and is not intended to provide, investment advice. Global Coin Report and/or its affiliates, employees, writers, and subcontractors are cryptocurrency investors and from time to time may or may not have holdings in some of the coins or tokens they cover. Please conduct your own thorough research before investing in any cryptocurrency and read our full disclaimer.

Image courtesy of Pxhere.com

Hong Kong, Hong Kong, 25th January, 2021, // ChainWire //

Xeno Holdings Limited (xno.live ), a blockchain solutions company based in Hong Kong, has announced the listing of its ecosystem utility token XNO on the ‘Bithumb Korea’ cryptocurrency exchange on January 21st 2021.

Xeno NFT Hub (market.xno.live ), developed by Xeno Holdings, enables easy minting of digital items into NFTs while also providing a marketplace where anyone can securely trade NFTs.

The Xeno NFT Hub project team includes former members of the technology project Yosemite X based in San Francisco and professionals such as Gabby Dizon who is a games industry expert and NFT space influencer based in Southeast Asia.

NFT(Non-Fungible Token) technology has recently gained huge focus in the blockchain arena and beyond, making waves in the online gaming sector, the art world, and the digital copyrights industry in recent years. The strongest feature of NFTs is that “NFTs are unique digital assets that cannot be replaced or forged”. Unlike fungible tokens such as Bitcoin or Ether, NFTs are not interchangeable for other tokens of the same type but instead each NFT has a unique value and specific information that cannot be replaced. This fact makes NFTs the perfect solution to record and prove ownership of digital and real-world items like works of art, game items, limited-edition collectibles, and more. One of the ways to have a successful…

2020 has been an incredible year for crypto as investors have generated windfall profits and crypto projects have seen their businesses gain the spotlight they’ve been looking for. While Bitcoin has received most of the attention after major institutional investors announced they were accumulating the increasingly scarce asset, many altcoins have also seen their fair share of glory. When looking at all the big winners of the past year, the first project that probably comes to mind is Chainlink, having appreciated by more than 550% YTD and now valued at over $4.5 billion. But, the actual biggest winner of the year is HEX with a YTD return of over 5,000%.

I mention both of the above projects as they have each taken slightly different paths to achieve greatness. Chainlink has devoted resources toward building a fundamentally sound business with many strategic partnerships while HEX has spent vast sums of money on marketing and promotion. Both approaches are valid, but one thing is certain, it is absolutely imperative for crypto projects to let the crypto community know what makes them special. Of course, one of the reasons that makes crypto so valuable is the powerful blockchain technology that most projects are utilizing.

Cryptocurrency vs. Blockchain Technology

It’s important to make a distinction between blockchain technology and cryptocurrency. Although they are often used interchangeably, they are different. Blockchain technology and crypto were both created after the 2008 financial crisis, but cryptocurrency…

Altcoins

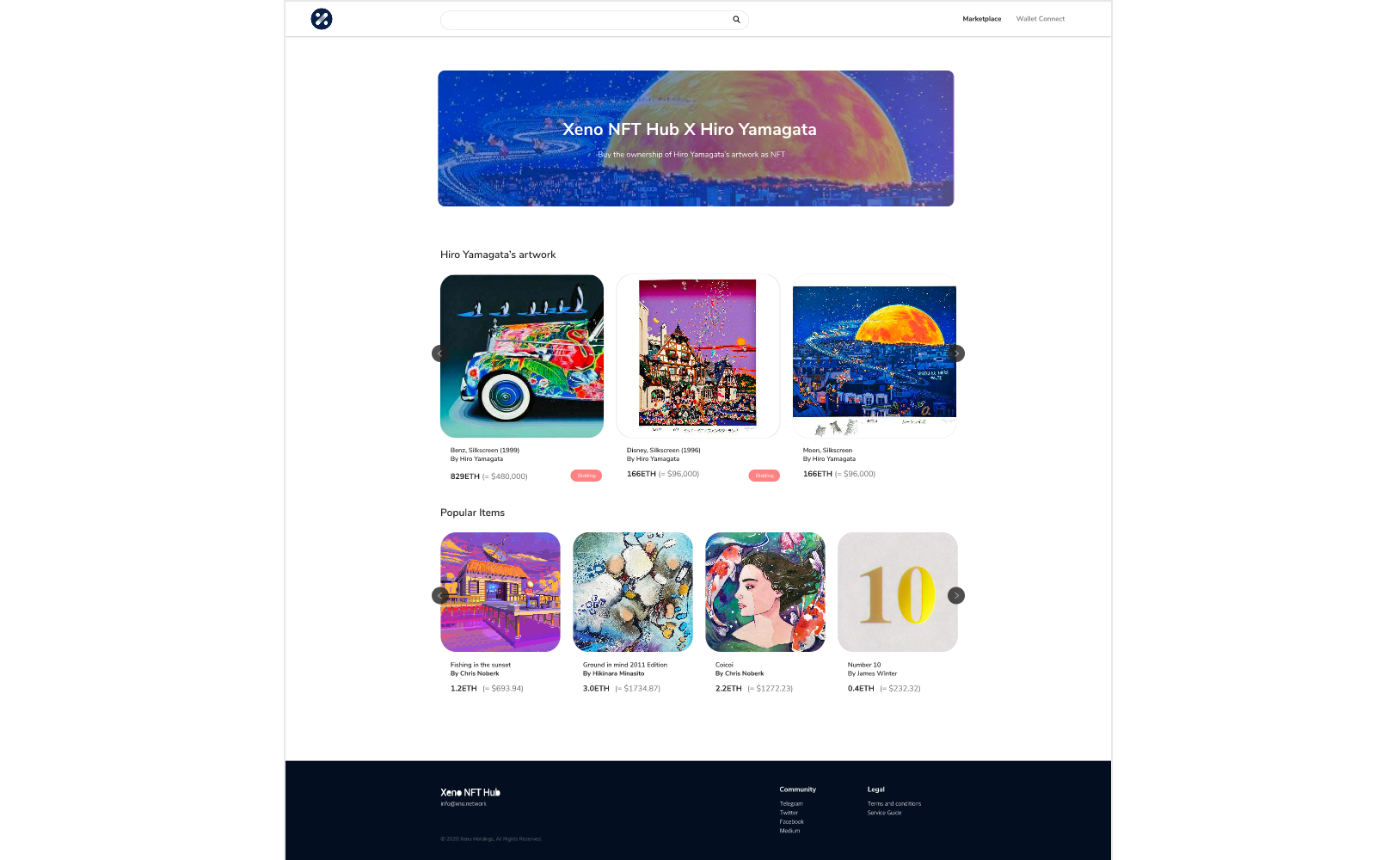

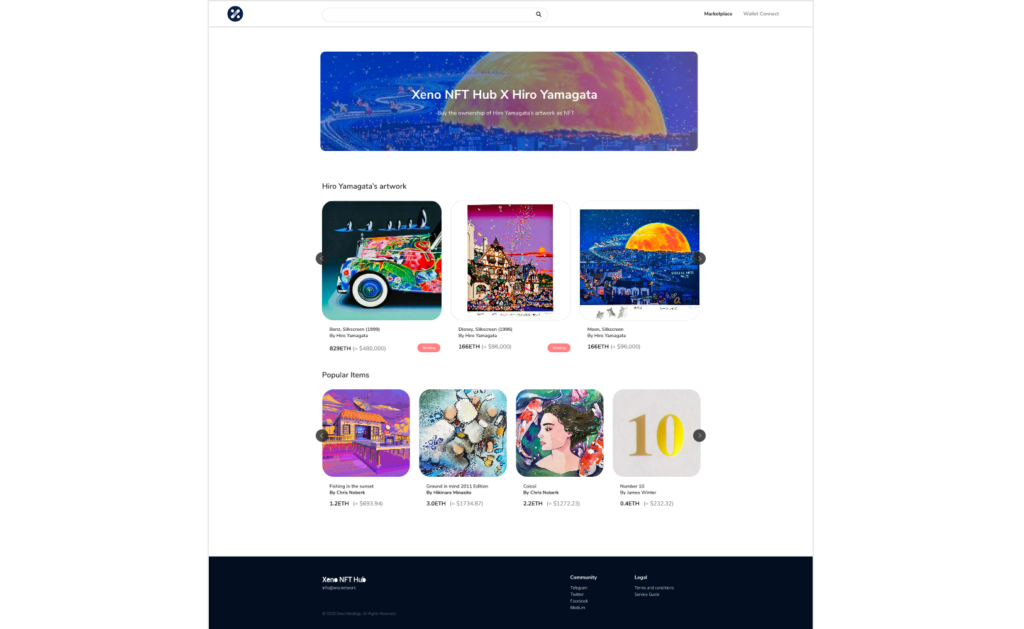

XENO starts VIP NFT trading service and collaborates with contemporary artist Hiro Yamagata

Hong Kong, Hong Kong, 24th December, 2020, // ChainWire //

The XENO NFT Hub (https://xno.live) will provide a crypto-powered digital items and collectables trading platform allowing users to create, buy, and sell NFTs. Additionally it will support auction based listings, governance and voting mechanisms, trade history tracking, user rating and other advanced features.

As a first step towards its fully comprehensive service, XENO NFT Hub launched a recent VIP service to select users and early adopters in December 2020 with plans for a full Public Beta to open in June 2021.

“NFTs are extremely flexible in their usage, from digital event tickets to artwork, and while NFTs have a very wide spectrum of uses and categories XENO will initially focus its partnership efforts and its own item curation on three primary areas: gaming, sports & entertainment, and collectibles.”, said XENO NFT Hub president Anthony Di Franco.

He also added “This does not mean we will prohibit other types of NFTs from our ecosystem However, it simply means that XENO’s efforts as a company will be targeted into these verticals initially as a cohesive business approach.”

Development and Procurement Lead, Gabby Dizon explained, “Despite our initial focus, we found ourselves with a unique opportunity to host some of the works of Mr. Hiro Yamagata. We are collaborating with Japanese artist Hiro Yamagata to enshrine some of his artwork into NFTs.”

Mr. Yamagata has…

-

Blogs7 years ago

Blogs7 years agoBitcoin Cash (BCH) and Ripple (XRP) Headed to Expansion with Revolut

-

Blogs7 years ago

Blogs7 years agoAnother Bank Joins Ripple! The first ever bank in Oman to be a part of RippleNet

-

Blogs7 years ago

Blogs7 years agoStandard Chartered Plans on Extending the Use of Ripple (XRP) Network

-

Blogs7 years ago

Blogs7 years agoElectroneum (ETN) New Mining App Set For Mass Adoption

-

Don't Miss7 years ago

Don't Miss7 years agoRipple’s five new partnerships are mouthwatering

-

Blogs7 years ago

Blogs7 years agoCryptocurrency is paving new avenues for content creators to explore

-

Blogs7 years ago

Blogs7 years agoEthereum Classic (ETC) Is Aiming To Align With Ethereum (ETH)

-

Blogs7 years ago

Blogs7 years agoIs Litecoin (LTC) Changing Its Game Plan By Going For Mass Adoption?