Blogs

Ripple (XRP) might not get adopted in mass, and here’s why

Ripple’s XRP crypto coin went all the way up to $3.50 this January thus achieving its historic peak value propelled by rumors of an imminent Coinbase listing. That brought it a lot of attention (CNBC even published an investor guide for acquiring XRP), but it also created controversy about the corporation, its marketing strategy, the token, and its real-world usefulness.

What does Ripple mean, anyway?

Ripple is not a monolithic notion. It actually encompasses three different entities that, while closely linked to each other, are quite different, and if we’re going to understand Ripple’s current situation we need to know what the differences are. First of all, there’s Ripple Inc., based in California. This is the corporation that is behind all the technology and the coin.

Then there’s the Ripple Protocol which is a blockchain based technology designed for inter-bank transfers and communications. The third concept related to Ripple is its coin, called XRP. That’s the company’s cryptocurrency.

The thing to keep in mind here is that Ripple’s banking platform does not require for its users to adopt the XRP coin in transfers, as it works using other currencies as well. But if they do adopt Ripple’s coin, things run faster and cheaper.

XRP is needed to pay the Ripple Protocol’s fees or as a bridge currency between different banks or within the same bank doing an international transaction.

The Ripple Protocol is sound and could really supplant the traditional way in which inter-bank operations work, which would have a substantial economic impact on the world. But that’s all about the protocol, not the coin. It remains unclear how big a role the XRP will play on this if any at all.

How banks do the trick

Let’s have a look at the Ripple Protocol. To understand it, we need to know how banks work in the 21st century. Let’s say I go to Banco Santander, which for example is my personal bank, and I deposit $10 into my savings account. By doing this, I am loaning $10 to Santander with the understanding that I will be repaid any time I ask. So Santander adds a $10 entry to their liabilities.

Let’s say I transfer that same money to a friend who also does his business at Santander. The bank’s balance doesn’t change, all that happens is that the same liability is now owed to him instead of me. The bank, of course, keeps an internal ledger that records all these debts to its clients.

If I want to send money to somebody who banks with a different institution, things get a bit more complicated because both banks need to keep their ledgers up to date and, at some point, my bank is going to have to make an actual payment to his bank.

Every country’s big players usually know each other well and trust each other (or at least work together all the time), so they are willing to make things faster for clients by accepting to issue IOUs and settling them at a future date.

That is possible as long as the banks trust each other, but they don’t always do. In that case, clients must wait for money to change hands among them or to be routed by a third party that is trusted by both banks. This takes time.

Over the last day I’ve asked several people close to banks if banks are indeed planning to begin using Ripple’s token, XRP, in a serious way, which is what investors seem to assume when they buy in at the current XRP prices. This is a sampling of what I heard back: pic.twitter.com/zbfMqg4TpD

— Nathaniel Popper (@nathanielpopper) January 5, 2018

Now let’s say that I want to send funds to a friend who lives in Taiwan and our banks do not trust each other. Maybe they’ve never even heard about each other. This is the most frequent scenario in international transactions. In this case, the money will follow a difficult route that will include several other institutions; it’s expensive, slow, error-prone.

It also needs for my bank to have my friend’s currency in reserve and for my friend’s bank to have my currency in reserve too. This increases both banks working capital needs, which is not great news for either bank because this kind of reserves are useless to them until somebody asks for a transaction between them which could be not a very frequent event.

The Ripple Protocol in a nutshell

In the Ripple Protocol, all participating banks are included in a single ledger (the Ripple Ledger). This makes things considerably faster and also means that these banks don’t need that frozen working capital anymore.

The network finds the shortest possible path for the money to follow by determining trust lines between the network. Because it’s based on a blockchain, it creates a distributed ledger globally that keeps the record of every transaction.

In these way, the decentralized ledgers allow banks to exchange IOUs to be settled in the future, and they can do it using fiat money, XRP, or any other digital asset.

While XRP doesn’t necessarily need to be the means of exchange, it’s still required to pay the network’s fees, and every user must keep at least 20 XRP tokens in their digital wallets if they want to transact. XRP is a deflationary currency

So what’s the point in keeping XRP tokens?

So once you’ve understood the protocol you must have realized this: however widely adopted the Ripple Protocol becomes, that doesn’t mean that XRP’s value will grow proportionally, which is why it’s so important to understand that coin and protocol are different animals.

XRP’s value will go up as its demand grows. That demand would come as banks use it as a bridge asset within the Ripple network to settle their business. But because XRP has shown some volatility, participants are not that sure they want that additional risk.

They know that using XRP in this way makes the network work better for them by reducing costs and increasing transaction speeds. But even with those incentives in the mix, it still makes better sense for them to use a more stable cryptocurrency to settle their debts.

As transactions within the net need fees to be paid in XRP, the demand will increase for sure as the protocol’s adoption increases, but this is going to be a very slow process, best case scenario.

As the use of decentralized exchanges becomes more common, it makes it easier to trade in all kinds of tokens quickly and safely, exposure to volatility decreases. This makes XRP something of a third wheel. It just adds friction to the user experience, and you can avoid it but only if you just have the funds, you need to complete the transaction.

The Ripple Protocol is actually a good one, so it makes things quicker and cheaper for banks even if they don’t use XRP to transact. Yes, if they do adopt XRP things do improve. But are they so much less expensive and quicker so the additional risk is worth taking?

Ripple allows settling accounts in many different currencies both fiat and digital. So the chances are that some fiat currency will be the main bridge for some time yet and that members will adopt a cryptocurrency (a very stable one) in the long-term.

Don’t try to run before you can walk

As things stand right now, it seems that banks and financial institutions’ current priority is not to have increased transaction speeds.

When you upgrade an internet user from dial-up internet to WiFi, they see the benefits immediately, but it will also make it harder to sell them a much faster service too soon, or at least until they’ve learned to use their new WiFi to its maximum.

Something like that also happened when cars appeared in the market. Horses were still around for a very long time, and one of the priorities back then was to make sure that the new machines did not scare the animals.

Banks are usually very conservative institutions in which inertia and skepticism hold changes back. They will make sure they can walk before they even consider attempting to run. Just adopting the Ripple Protocol (let alone the coin) is already a significant change for them.

Even Ripple’s Chief Cryptographer, David Schwarz, has made it clear that the Ripple Protocol is powerful enough to work without XRP. Even without any blockchain at all. It improves international payments so much over the current legacy systems that banks will adopt it even if, in the end, fiat money keeps moving just as it does right now.

Mr. Schwarz also said that the tricky bit in all this is to get banks to use the blockchain but that it’s not the blockchain per se that makes the network convenient but the integration with current systems, compliance, and governance. And that’s what Ripple does. But if transactions costs go down even by a cent by adopting XRP, it still makes sense to adopt it, according to him.

In his opinion, Ripple’s and XRP advantages speak for themselves. If he’s right, XRP’s value will increase very much very quickly.

XRP: The skeptics

Skeptics think that XRP shouldn’t exist in the Ripple Protocol at all. They just see no reason for that other than to make users buy XRP tokens thus inflating XRP’s price in the open market without really adding any value.

“Ripple is highly centralized & XRP is more akin to a PayPal account than a trustless system like bitcoin…. It's hard to come up w any rational reason why XRP exists in the Ripple protocol, other than as a means for Ripple to make money. Lots of money.“ https://t.co/c52yl5joiG

— Laura Shin (@laurashin) January 4, 2018

There are 100 billion XRP tokens in existence, and they are all already mined and ready to sell as the mining process was completed before the protocol was launched. Last December Ripple committed to storing 55 billion XRP tokens in a crypto-safe escrow account to make everybody know that the token’s supply is not at risk. A billion XRP are released from this vault on a monthly basis for Ripple to use as they deem fit. So far, it’s been mainly to create market incentives and sell to institutional investors.

Ripple has used those funds responsibly so far. They’ve sold about 30% monthly, and any XRP remainings go into a new escrow account.

It currently seems that XRP’s prices are inflated. Investors speculate that XRP will indeed become a global currency that will facilitate transactions between banks. Such event will disrupt a worldwide trillion dollar industry, and XRP would be at the heart of it. This is the belief (or hope) that is driving XRP’s price up.

But this doesn’t need to happen because the Protocol doesn’t really need to use the coin, except for fees, and fees will not create such high demand. Also, banks will not go for XRP until they are sure that it’s a stable asset.

We are quite optimistic about Ripple as a project. Many banks are adopting it, and that’s just a significant step for the whole blockchain industry. It will revitalize an industry that sorely needs it, but that’s the Protocol. On the other hand, to buy and keep XRP tokens as a retail investor, in long-term, doesn’t make much sense as yet. Wait a bit further at this stage, judge, and then invest (if you want to)!

For the latest cryptocurrency news, join our Telegram!

Disclaimer: This article should not be taken as, and is not intended to provide, investment advice. Global Coin Report and/or its affiliates, employees, writers, and subcontractors are cryptocurrency investors and from time to time may or may not have holdings in some of the coins or tokens they cover. Please conduct your own thorough research before investing in any cryptocurrency and read our full disclaimer.

Image courtesy of Pxhere.com

Hong Kong, Hong Kong, 25th January, 2021, // ChainWire //

Xeno Holdings Limited (xno.live ), a blockchain solutions company based in Hong Kong, has announced the listing of its ecosystem utility token XNO on the ‘Bithumb Korea’ cryptocurrency exchange on January 21st 2021.

Xeno NFT Hub (market.xno.live ), developed by Xeno Holdings, enables easy minting of digital items into NFTs while also providing a marketplace where anyone can securely trade NFTs.

The Xeno NFT Hub project team includes former members of the technology project Yosemite X based in San Francisco and professionals such as Gabby Dizon who is a games industry expert and NFT space influencer based in Southeast Asia.

NFT(Non-Fungible Token) technology has recently gained huge focus in the blockchain arena and beyond, making waves in the online gaming sector, the art world, and the digital copyrights industry in recent years. The strongest feature of NFTs is that “NFTs are unique digital assets that cannot be replaced or forged”. Unlike fungible tokens such as Bitcoin or Ether, NFTs are not interchangeable for other tokens of the same type but instead each NFT has a unique value and specific information that cannot be replaced. This fact makes NFTs the perfect solution to record and prove ownership of digital and real-world items like works of art, game items, limited-edition collectibles, and more. One of the ways to have a successful…

2020 has been an incredible year for crypto as investors have generated windfall profits and crypto projects have seen their businesses gain the spotlight they’ve been looking for. While Bitcoin has received most of the attention after major institutional investors announced they were accumulating the increasingly scarce asset, many altcoins have also seen their fair share of glory. When looking at all the big winners of the past year, the first project that probably comes to mind is Chainlink, having appreciated by more than 550% YTD and now valued at over $4.5 billion. But, the actual biggest winner of the year is HEX with a YTD return of over 5,000%.

I mention both of the above projects as they have each taken slightly different paths to achieve greatness. Chainlink has devoted resources toward building a fundamentally sound business with many strategic partnerships while HEX has spent vast sums of money on marketing and promotion. Both approaches are valid, but one thing is certain, it is absolutely imperative for crypto projects to let the crypto community know what makes them special. Of course, one of the reasons that makes crypto so valuable is the powerful blockchain technology that most projects are utilizing.

Cryptocurrency vs. Blockchain Technology

It’s important to make a distinction between blockchain technology and cryptocurrency. Although they are often used interchangeably, they are different. Blockchain technology and crypto were both created after the 2008 financial crisis, but cryptocurrency…

Altcoins

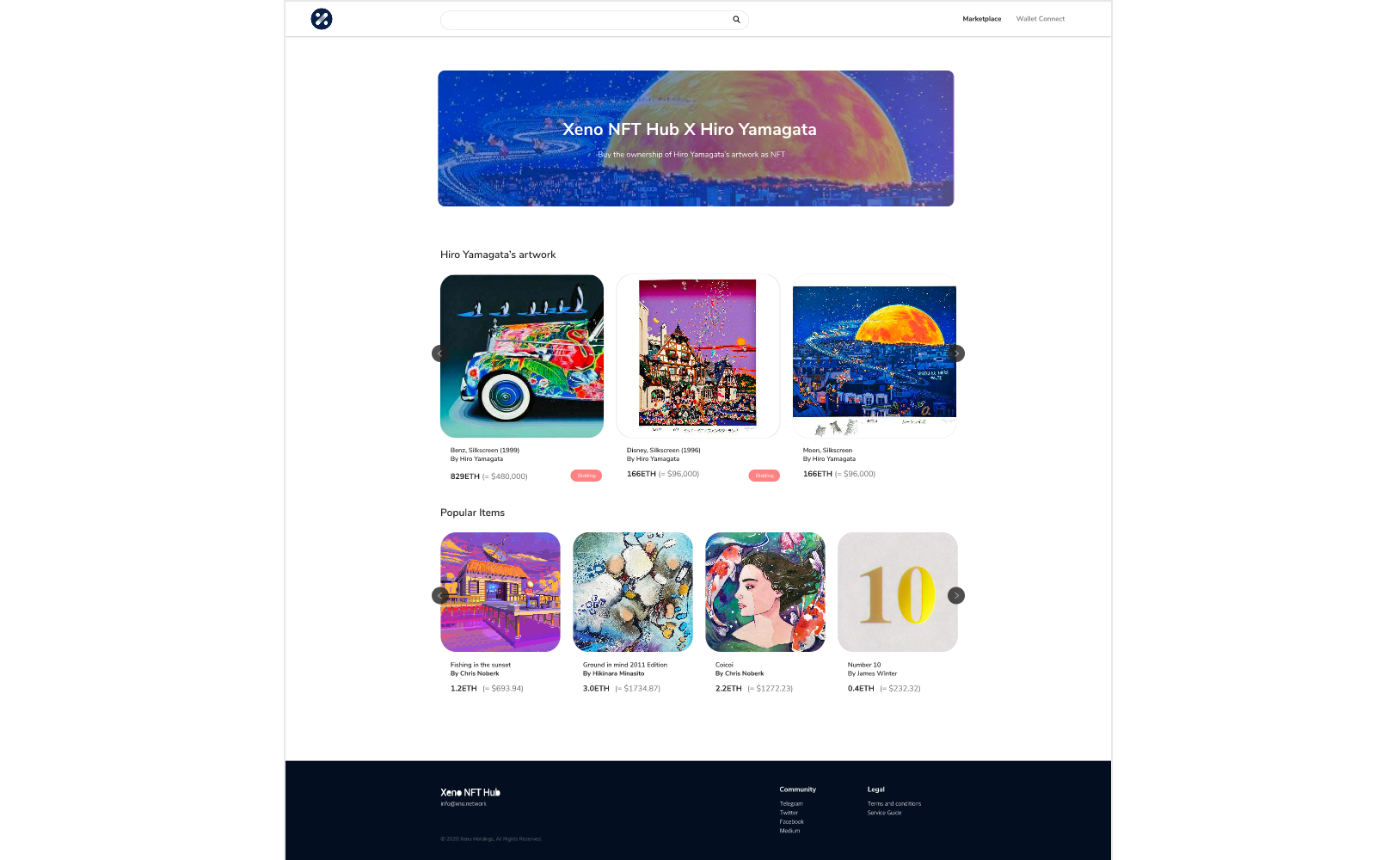

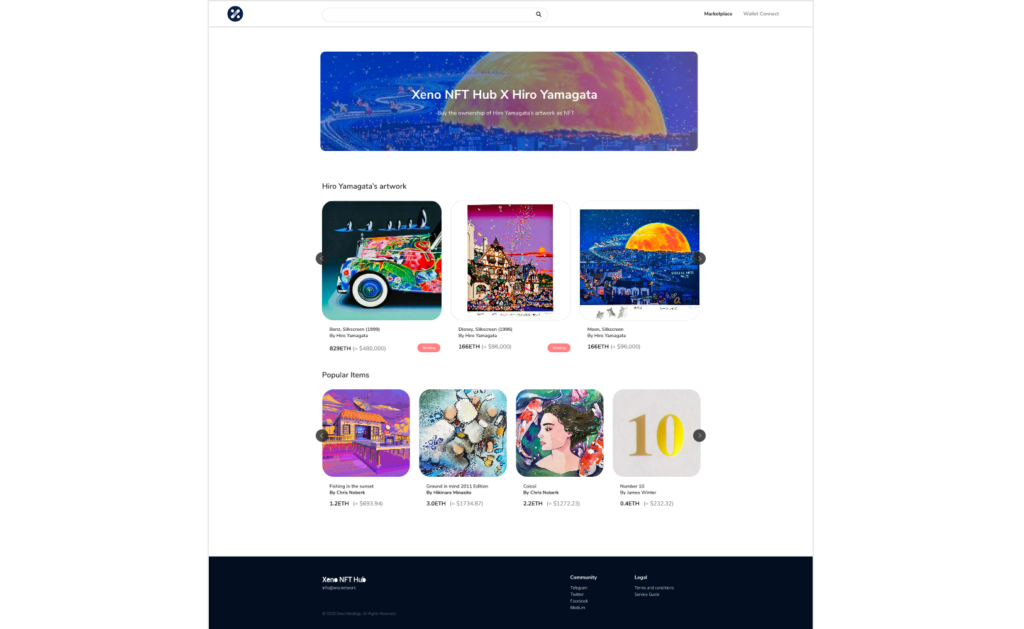

XENO starts VIP NFT trading service and collaborates with contemporary artist Hiro Yamagata

Hong Kong, Hong Kong, 24th December, 2020, // ChainWire //

The XENO NFT Hub (https://xno.live) will provide a crypto-powered digital items and collectables trading platform allowing users to create, buy, and sell NFTs. Additionally it will support auction based listings, governance and voting mechanisms, trade history tracking, user rating and other advanced features.

As a first step towards its fully comprehensive service, XENO NFT Hub launched a recent VIP service to select users and early adopters in December 2020 with plans for a full Public Beta to open in June 2021.

“NFTs are extremely flexible in their usage, from digital event tickets to artwork, and while NFTs have a very wide spectrum of uses and categories XENO will initially focus its partnership efforts and its own item curation on three primary areas: gaming, sports & entertainment, and collectibles.”, said XENO NFT Hub president Anthony Di Franco.

He also added “This does not mean we will prohibit other types of NFTs from our ecosystem However, it simply means that XENO’s efforts as a company will be targeted into these verticals initially as a cohesive business approach.”

Development and Procurement Lead, Gabby Dizon explained, “Despite our initial focus, we found ourselves with a unique opportunity to host some of the works of Mr. Hiro Yamagata. We are collaborating with Japanese artist Hiro Yamagata to enshrine some of his artwork into NFTs.”

Mr. Yamagata has…

-

Blogs7 years ago

Blogs7 years agoBitcoin Cash (BCH) and Ripple (XRP) Headed to Expansion with Revolut

-

Blogs7 years ago

Blogs7 years agoAnother Bank Joins Ripple! The first ever bank in Oman to be a part of RippleNet

-

Blogs7 years ago

Blogs7 years agoStandard Chartered Plans on Extending the Use of Ripple (XRP) Network

-

Blogs7 years ago

Blogs7 years agoElectroneum (ETN) New Mining App Set For Mass Adoption

-

Don't Miss7 years ago

Don't Miss7 years agoRipple’s five new partnerships are mouthwatering

-

Blogs7 years ago

Blogs7 years agoCryptocurrency is paving new avenues for content creators to explore

-

Blogs7 years ago

Blogs7 years agoEthereum Classic (ETC) Is Aiming To Align With Ethereum (ETH)

-

Blogs7 years ago

Blogs7 years agoIs Litecoin (LTC) Changing Its Game Plan By Going For Mass Adoption?